Mold Remediation Insurance Claims Guide

For Nash Everett Customers

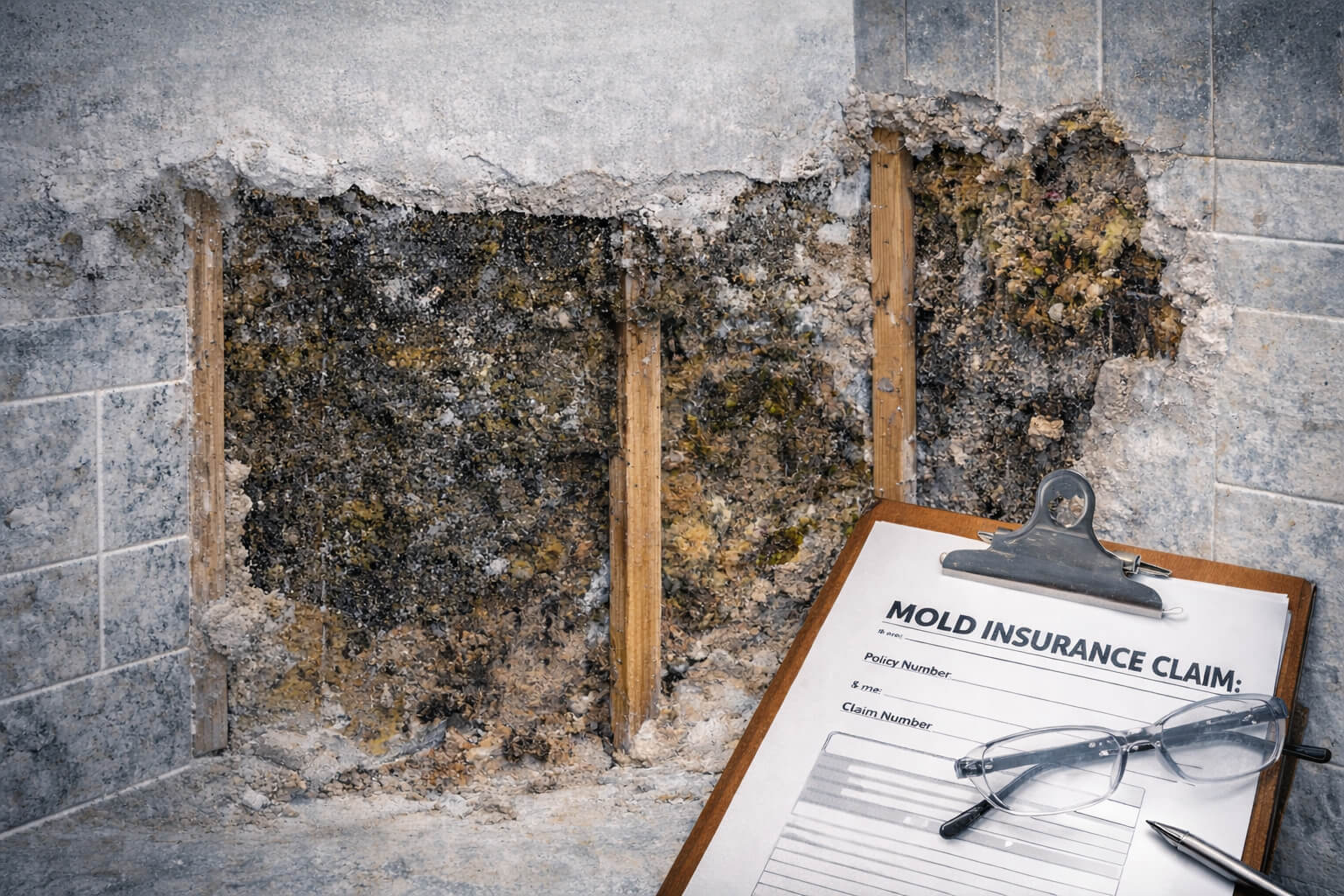

At Nash Everett, we understand that discovering mold in your home can be stressful, especially when you are unsure whether your insurance policy will cover remediation. This guide is designed to help you better understand the insurance claim process and what steps you can take when mold or water damage occurs.

Please note:

- Nash Everett does not work directly for insurance companies and cannot provide legal advice regarding insurance claims.

- Insurance policies vary widely, and coverage depends on the specific terms of your policy.

However, we are happy to assist our customers by providing documentation, photos, inspection reports, and remediation records that may help support your claim.

Understanding Mold Coverage in Home Insurance

- Many homeowners are surprised to learn that mold itself is rarely covered unless it is caused by a covered water event.

- Insurance companies typically look at the source of the moisture when deciding whether a claim is valid.

Mold is often covered when it results from:

- Sudden plumbing failures (burst pipes)

- Water heater leaks or failures

- Appliance failures (dishwashers, washing machines)

- Accidental water discharge

- Storm damage that allows water into the home

- Ice dams or roof damage from storms

- Firefighting water damage

Mold is often NOT covered when caused by:

- Long-term leaks

- Maintenance issues

- Humidity or ventilation problems

- Crawlspace moisture over time

- Gradual roof leaks

- Flooding without flood insurance

- Neglected repairs

Many policies include limited mold coverage caps, commonly ranging from $1,000 to $10,000, although this varies.

Water vs. Flood Damage

Understanding the difference can impact your claim.

Water Damage (Often Covered)

This refers to sudden and accidental water events inside the home, such as:

- Burst pipes

- Overflowing appliances

- Plumbing failures

- Water heater failures

Flood Damage (Usually NOT Covered)

- Flooding from outside water entering the home is generally not covered by standard homeowners insurance.

- Flood coverage typically requires a separate policy through programs such as the National Flood Insurance Program.

- Flood damage examples include:

- Storm surge

- Rising groundwater

- River overflow

- Heavy rain entering the structure from outside

Steps to Take When Mold or Water Damage is Discovered

1. Document Everything

- Before cleanup begins, collect evidence.

- Take photos and videos of:

- Visible mold growth

- Water damage

- Leaks or plumbing failures

- Damaged building materials

- Moisture readings (if available)

Nash Everett can assist by providing:

- Inspection photos

- Moisture readings

- Remediation documentation

- Work reports

These documents may be helpful during the claims process.

2. Review Your Insurance Policy

- Look for sections related to:

- Water damage

- Mold remediation limits

- Sudden and accidental discharge

- Exclusions

- Flood coverage

Important terms to search for include:

- “Resulting damage”

- “Sudden and accidental”

- “Hidden water damage”

- “Mold sub-limits”

3. Contact Your Insurance Company

Report the claim as soon as possible.

Provide:

- Policy number

- Date damage was discovered

- Description of the event

- Photos and documentation

- Keep notes of:

- Claim number

- Adjuster contact information

- Dates of communication

Tips for Speaking With Insurance Adjusters

- Insurance adjusters evaluate claims based on policy language and cause of loss.

- How the situation is described can sometimes affect how a claim is interpreted.

- Helpful Language to Use

- Focus on sudden events and when you discovered the issue.

Examples:

“We discovered water damage on (date).”

“There appears to have been a plumbing failure.”

“The issue was not visible until recently.”

“The damage appears to be from a sudden leak.”

Language to Avoid

Avoid statements that imply long-term neglect or known ongoing issues.

Examples to avoid:

- “This leak has probably been happening for years.”

- “We knew about the problem but didn’t fix it yet.”

- “There has always been moisture in this area.”

If you are unsure about the cause, it is acceptable to say:

- “We are not certain of the cause yet.”

Working With the Adjuster

- When the adjuster visits your home:

- Walk them through the affected areas

- Provide any documentation you have

- Share photos and reports from Nash Everett

- Ask questions about your coverage

You can also ask the adjuster:

- “Is mold remediation included under my policy?”

- “What documentation do you need to evaluate this claim?”

- “Is there a coverage limit for mold remediation?”

How Nash Everett Can Help

While we do not work directly for insurance companies, we can assist our customers by providing:

- Mold inspection findings

- Photos of contamination and damage

- Moisture readings

- Scope of remediation

- Post-remediation documentation

- Invoices and service records

These materials may help support your claim when communicating with your insurance provider.

If Your Claim Is Denied

A claim denial does not always mean the process is over.

Some homeowners choose to pursue additional options such as:

- Requesting a Policy Review

- Ask your insurance company to explain the denial and reference the exact policy language used.

Filing an Appeal

Many insurance companies allow formal claim appeals with additional documentation.

Hiring a Public Adjuster

A public adjuster works on behalf of the homeowner to evaluate and negotiate claims.Public adjusters are licensed professionals who may review your policy and damage independently.

Consulting an Insurance Attorney

If significant damage or claim value is involved, some homeowners choose to consult an attorney experienced in insurance claims.

Preventing Future Mold Issues

Insurance companies often evaluate whether reasonable steps were taken to prevent damage.

Helpful preventative measures include:

- Addressing plumbing leaks quickly

- Maintaining roof and gutters

- Controlling humidity with dehumidifiers

- Proper crawlspace encapsulation

- Adequate attic ventilation

- Regular home inspections

- These measures can reduce the risk of future mold problems.

Our Commitment to Our Customers

At Nash Everett, our focus is on providing professional mold remediation and indoor environmental solutions for New Jersey homeowners.

We are committed to:

- Honest assessments

- Proper remediation practices

- Clear documentation

- Helping customers navigate the process as smoothly as possible